Uranium Basic Statistics

Last updated: 2025-02-24

Compiled from WNA / OECD-NEA and selected public supplements. Domestic U.S.-only notes are excluded where possible.

1. Highlights & Overview

- World production (2024) is approximately 71,006 tU.

- Global reserves are approximately 5,925,700 tU.

- The largest producer is Kazakhstan, accounting for about 32.8% of global output.

- In 2024, Kazakhstan ranked among the top producers (23,270).

- The top 3 countries account for about 63.3% of global output, indicating concentrated supply.

- Source: WNA World Uranium Mining Production

- Source: WNA Supply of Uranium

- Source: WNA Reactors and Uranium Requirements

- Source: OECD/NEA Red Book (Uranium: Resources, Production and Demand)

2. Price Trends & Global Market (Events, Trends, and Issues)

- Key market highlights are currently being prepared.

No quantitative usage breakdown (global basis) was found in the source text for this year.

3. World Mine Production and Reserves

Top Producing Countries(2024, Top 5)

Top Reserves (Top 5)

| Country | Production(2024) | Reserves |

|---|---|---|

| Kazakhstan | 23,270 | 813,900 |

| Canada | 14,309 | 582,000 |

| Namibia | 7,333 | 497,900 |

| Australia | 4,598 | 1,671,200 |

| Uzbekistan | 4,000 | |

| Russia | 2,738 | 476,600 |

| China | 1,600 | 270,500 |

| Niger | 962 | 336,000 |

| India | 500 | |

| Ukraine | 288 | 106,700 |

| USA | 260 | 67,800 |

| South Africa | 200 | 320,900 |

Unit: tU

4. Supply-Demand Balance Trend

Unit: tU / Positive values indicate supply surplus; negative values indicate supply deficit.

5. Metallurgical & Physical Properties and Industrial Uses

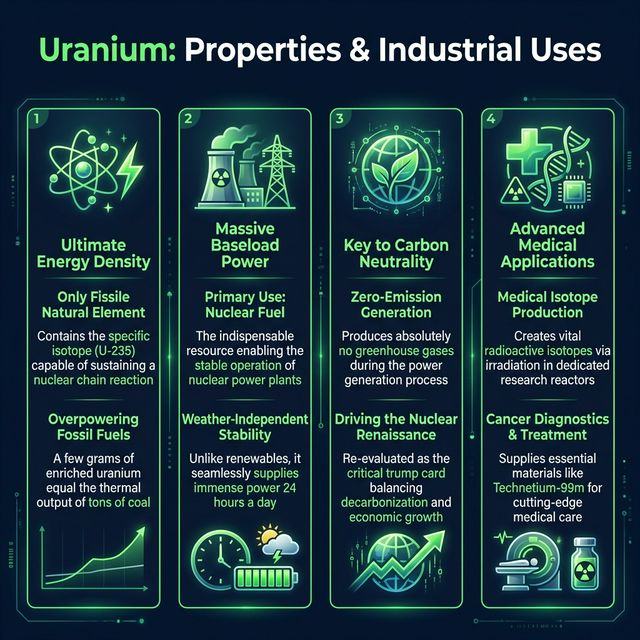

Uranium (U) is a radioactive metal belonging to the actinide series and is among the heaviest naturally occurring elements. It is a silvery-white, extremely dense metal (19.1 g/cm³), and it readily oxidizes in the air to become covered with a black oxide film. The most prominent metallurgical or rather atomic-physical characteristic of uranium is that it is the only naturally occurring element that contains an isotope (Uranium-235, with a natural abundance of approximately 0.72%) capable of sustaining a nuclear fission chain reaction [49].

Due to this fissile property, uranium possesses an astronomical energy density that is orders of magnitude greater than that of fossil fuels. Just a few grams of enriched uranium release energy equivalent to the combustion of several tons of coal [49]. Consequently, the sole and absolute primary industrial application of uranium is as nuclear fuel for nuclear power plants [49].

Whereas renewable energy sources like solar and wind are intermittent power sources dependent on weather and time of day, nuclear power is a "baseload power source" capable of continuously and stably supplying massive amounts of electricity over periods of months to years, independent of the weather [49]. Because it emits no greenhouse gases (CO2) during the power generation process, countries like China and many others are accelerating the new construction and restarting of nuclear power plants as a trump card to achieve both decarbonization (carbon neutrality) and economic growth [49].

Beyond power generation, uranium also plays an extremely critical role as a target material. By irradiating uranium in commercial power reactors or dedicated research reactors, it is used to produce radioisotopes (such as Molybdenum-99, the parent nuclide of Technetium-99m) that are utilized in the medical field for cancer diagnosis and treatment [50].

6. Structural Issues Governing Supply and Demand

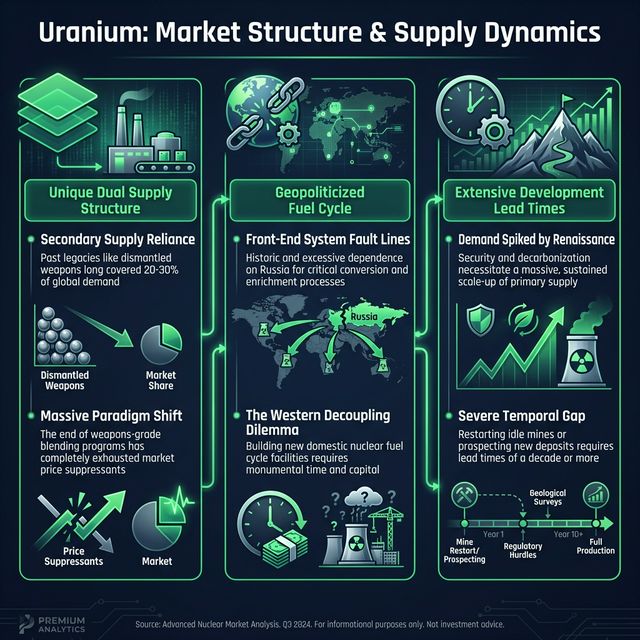

The supply-demand mechanism of the uranium market operates on an anomalous "dual structure" that is completely different from any other mineral commodity.

The greatest special circumstance dominating the uranium market is its historical background, where supply is divided into "primary supply" (mine production) and "secondary supply," with the latter having exerted a massive influence on market prices [51]. Uranium secondary supply refers to sources of uranium other than newly mined material. Specifically, it consists of the following four main elements:

1. Down-blending of Weapons-Grade Highly Enriched Uranium (HEU): Programs (such as the "Megatons to Megawatts" program) that dismantle highly enriched uranium piled up by the U.S. and Russia during the Cold War for nuclear weapons, dilute it into low-enriched uranium (LEU) for civilian power generation, and release it into the market [51]. 2. Underfeeding at Enrichment Plants: In the uranium enrichment process, during periods when there is spare operational capacity, extra enrichment work is performed to conserve the amount of natural uranium fed into the process. The saved natural uranium is then sold on the market [51]. 3. Tails Re-enrichment: A method of using modern technology to re-extract the trace amounts of Uranium-235 remaining in depleted uranium (tails) discarded during past enrichment processes [50]. 4. Drawdown of Commercial and Government Inventories: The release of strategic stockpiles held by power utilities and national government agencies into the market [51].

From the 1990s through the 2010s, 20% to 30% of the uranium demand required by the world's nuclear reactors was met by this "secondary supply," a legacy of the past [52]. Consequently, for a long time, uranium was supplied at cheap prices that fell below the cost of primary supply (mine production), eroding the incentive for mine development. However, today, the megaton-class HEU supply from nuclear weapons dismantling programs is nearing its end, and the share of secondary supply is dramatically declining (depleting) [50]. The paradigm shift caused by the disappearance of this secondary supply is the fundamental reason pushing up uranium spot prices.

The second special circumstance is the fragmentation of the highly politicized "front-end supply chain." After being mined, uranium cannot be loaded into a reactor until it undergoes a series of processes (the front end of the nuclear fuel cycle): milling (conversion into yellowcake), conversion (chemical transformation into uranium hexafluoride), enrichment (increasing the ratio of Uranium-235), and fuel fabrication [56]. While Kazakhstan, Canada, and Australia hold top shares in mine production, for the conversion and enrichment processes, Western countries have historically relied heavily on the massive capacity of Russia's state-owned corporation (Rosatom) [57]. Following Russia's invasion of Ukraine in 2022, Western nations have rushed to break their dependence on Russian nuclear fuel from an economic security standpoint (via embargoes and tariffs) [52]. However, constructing new domestic enrichment and conversion facilities, or expanding their capacities, requires enormous time and capital investment, making short-term substitution extremely difficult. The anxiety over supply chain restructuring stemming from this geopolitical fault line has acted as the direct trigger fanning supply fears and causing prices to soar [52].

Furthermore, on the demand side—after a prolonged period of stagnation (slumping prices and frozen investment in new mines) following the Fukushima Daiichi nuclear disaster—an increase in demand driven by a global nuclear renaissance is now viewed as certain. To fill the gap left by depleting secondary supply and satisfy new demand, new uranium mines must be urgently developed to launch "primary supply" on a massive scale. Yet, restarting idled mines or exploring new ones requires lead times on the order of decades [52]. The fear of medium-to-long-term supply deficits caused by this temporal gap shapes the current reality of the uranium market.

References

- [49] The Impact of Uranium Resource Constraints on China\'s Nuclear Power Development

- [50] Management of high enriched uranium for peaceful purposes: Status and trends

- [51] Supply of Uranium - World Nuclear Association

- [52] Uranium 2024: Resources, Production and Demand - Nuclear Energy Agency (NEA)

- [56] Nuclear Power and the Uranium Market: Are Reserves and Resources Sufficient? - DIW Berlin

- [57] Global uranium market dynamics: analysis and future implications - ResearchGate