Palladium Basic Statistics

Last updated: 2025-02-24

Compiled from USGS MCS 2026 and selected public supplements. Domestic U.S.-only notes are excluded where possible.

1. Highlights & Overview

- World production (2025) is approximately 190,000 kg (PGM contained).

- Global reserves are approximately 76,000,000 kg (PGM contained).

- The largest producer is Russiae, accounting for about 44.2% of global output.

- In 2025, Russiae ranked among the top producers (84,000).

- The top 3 countries account for about 89.5% of global output, indicating concentrated supply.

- Source: USGS MCS 原文PDF

- Source: Johnson Matthey Palladium Supply & Demand

2. Price Trends & Global Market (Events, Trends, and Issues)

- In 2025, production of PGMs in South Africa, the world’s leading producer of PGM- containing mined material, decreased by an estimated 9% compared with that in 2024 owing to declining palladium prices, higher costs associated with deep-level mining, and ongoing disruptions to the supply of electricity.

- Estimated production in Russia, the world’s leading producer of mined palladium, decreased by 6% owing to lower metal grades and ore recovery, geopolitical and investor uncertainty related to the Russia-Ukraine conflict, and the introduction of new mining equipment at one operation.

- The estimated annual average price in 2025 increased by 53% for ruthenium, by 25% for platinum, by 24% for rhodium, and by 11% for palladium compared with the average prices in 2024.

- The estimated annual price of iridium decreased by 9% compared with annual average price in 2024.

Usage Mix (Based on Public Data)

3. World Mine Production and Reserves

Top Producing Countries(2025, Top 5)

Top Reserves (Top 5)

| Country | Production(2025) | Reserves |

|---|---|---|

| Russiae | 84,000 | 11,000,000 |

| South Africa | 70,000 | 63,000,000 |

| Canada | 16,000 | 310,000 |

| Zimbabwe | 15,000 | 1,300,000 |

| United States | 6,200 | 590,000 |

Unit: kg(PGM含有量)

4. Supply-Demand Balance Trend

Unit: koz / Positive values indicate supply surplus; negative values indicate supply deficit.

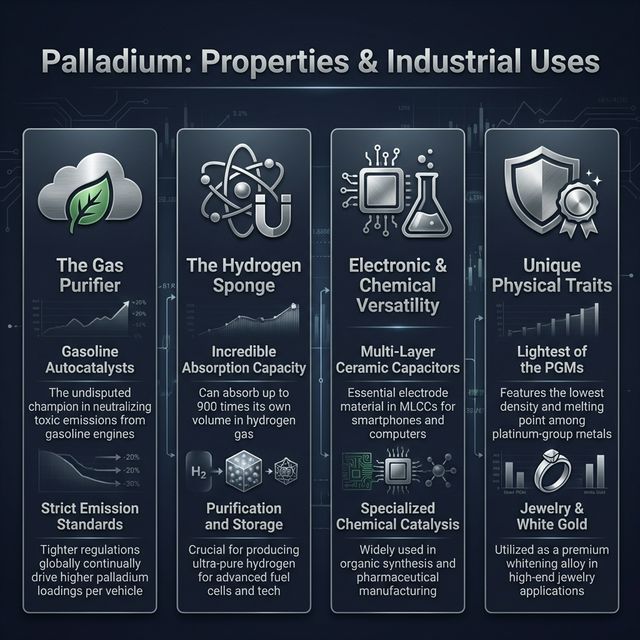

5. Metallurgical & Physical Properties and Industrial Uses

Palladium (Pd) is a Group 10 transition metal (PGM) alongside platinum, but compared to platinum, it has a lower density (12.02 g/cm³) and the lowest melting point among PGMs at 1,555°C. Metallurgically, its most unique property is its extraordinary "hydrogen absorption and permeation capability." Under standard temperature and pressure, palladium has the ability to absorb up to 900 times its own volume of hydrogen gas between its metal lattice to form a palladium hydride [23]. During this process, hydrogen molecules dissociate into atoms on the palladium surface, diffuse through the metal lattice, and recombine back into molecules on the opposite side.

One of the largest industrial applications leveraging this characteristic is palladium alloy membranes (membrane filters) used to purify ultra-high-purity hydrogen gas. In industries requiring hydrogen completely free of impurities, such as the semiconductor manufacturing process, palladium membranes play an irreplaceable role by completely blocking other gases while allowing only hydrogen to permeate [23].

However, the overwhelming majority (over 80%) of current palladium demand comes from three-way catalytic converters (autocatalysts) for gasoline-powered vehicles, capitalizing on its excellent catalytic activity much like platinum [30]. Palladium demonstrates extremely high efficiency in the process of simultaneously purifying carbon monoxide (CO), hydrocarbons (HC), and nitrogen oxides (NOx) contained in gasoline engine exhaust. In conjunction with the tightening of global emission regulations (such as Euro 6 and China VI), the palladium loading per vehicle has consistently increased [30].

Other applications include its use as an internal electrode material for multi-layer ceramic capacitors (MLCCs) in the electronics industry, its use in dental alloys due to its high biocompatibility, and its active role as homogeneous and heterogeneous catalysts in the chemical industry [19]. Notably, in the field of organic synthetic chemistry, it is an indispensable component for advanced fine chemical synthesis—such as pharmaceuticals and organic EL materials—serving as a catalyst for carbon-carbon bond forming reactions represented by the Suzuki-Miyaura coupling [19].

6. Structural Issues Governing Supply and Demand

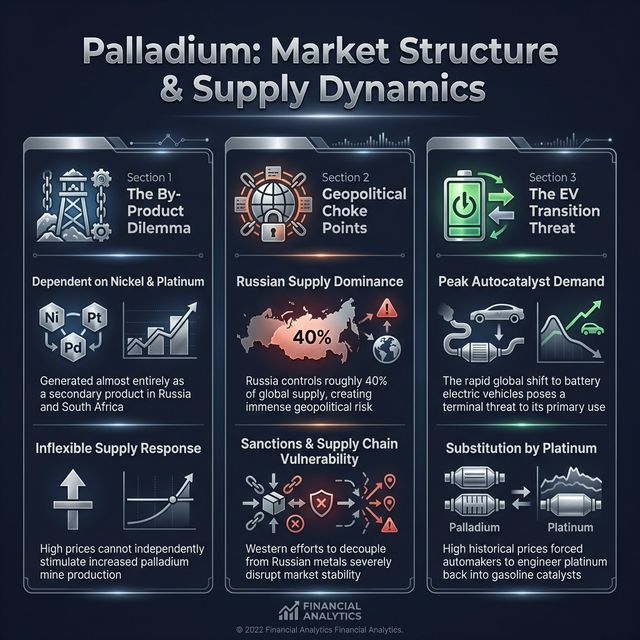

The supply and demand structure of palladium is characterized by three critical risk factors: "extreme dependence on a specific country (Russia)," "long-term demand destruction risk due to over-reliance on internal combustion engines," and the aforementioned "substitution dynamics with platinum."

First is geopolitical risk and the inelasticity of supply. Russia is the world's largest producer of palladium, solely accounting for approximately 40% of global supply [30]. In particular, Russian mining and metals giant Norilsk Nickel (PJSC MMC Norilsk Nickel) stands as the world's largest single corporate producer of palladium [30]. Since Russia's invasion of Ukraine, economic sanctions by Western nations and movements toward supply chain decoupling have brought extreme tension to the palladium market [30]. Moreover, it is crucial to note that palladium production in Russia is primarily conducted as a "by-product" accompanying nickel and copper mining [30]. Just as with silver, even if palladium demand surges and prices skyrocket, without corresponding strength in the market for its primary product (nickel), it is economically difficult for Norilsk Nickel to increase production solely for palladium. Consequently, the palladium market features a structurally inelastic supply, prone to extreme price volatility [30].

The second special circumstance is the future survival risk stemming from the singularity of its demand. Because palladium relies on gasoline vehicle exhaust catalysts for over 80% of its demand, it faces a "structural valley of death" where the majority of its demand could completely disappear in the long term if global decarbonization and the shift to battery electric vehicles (BEVs) progresses [30]. BEVs, which produce absolutely no exhaust gas, have no need for autocatalysts. However, the current market situation is somewhat complex. Due to factors like high BEV prices, inadequate charging infrastructure, and reduced battery performance in cold climates, consumers maintain psychological hurdles toward fully transitioning to BEVs. As a result, sales of hybrid electric vehicles (HEVs) and plug-in hybrid electric vehicles (PHEVs)—which combine a gasoline engine with a motor—have remained unexpectedly robust [30]. Interestingly, because hybrid vehicles frequently turn their engines on and off while driving, the catalyst temperature tends to drop below the optimal temperature for purification (activation temperature). To maintain exhaust purification performance during these "cold starts," hybrid vehicles paradoxically require a heavier palladium loading in their catalysts than pure gasoline vehicles. This phenomenon is currently serving as a short-to-medium-term underlying support factor for palladium demand [30].

Third is the historical background of substitution. From the 1990s through the early 2000s, faced with soaring platinum prices, automakers massively shifted their catalyst compositions from platinum to palladium, which was cheaper at the time [25]. However, the subsequent concentration of demand on palladium, coupled with supply fears from Russia (such as export delays in the early 2000s), led to a situation where palladium prices temporarily surpassed platinum [27]. Today, as palladium prices have remained elevated once again, a movement of "reverse substitution"—replacing palladium with platinum—has taken hold in the automotive industry. In 2024, it is estimated that about 700,000 ounces of palladium demand will be replaced by platinum [26]. Because the chemical formulation (mixing ratio) of a catalyst, once set, is difficult to revert quickly due to the barrier of regulatory certification, this substitution trend structurally continues to erode palladium demand over the medium term [26].

References

- [19] Investigation of mechanical and structural characteristics of platinum and palladium at high temperatures \| Revista de Metalurgia

- [23] Properties and Uses of Palladium \| Johnson Matthey Technology \...

- [25] A Review of Recovery of Palladium from the Spent Automobile Catalysts - MDPI

- [26] Platinum for palladium substitution is embedded into automotive demand and unlikely to reverse swiftly

- [27] Substitution among Platinum Group Metals - CME Group

- [30] Analysis of the Palladium Market: A Strategic Aspect of Sustainable \...